Related Articles

Business interruption and cyber incidents are the primary concerns for the manufacturing sector within the automotive industry in 2024, according to the Allianz Risk Barometer. The report, based on insights from over 3,000 risk management professionals and business leaders, highlights the growing importance of addressing these risks to ensure business continuity and safeguard against potential disruptions.

Business interruption and cyber incidents are the primary concerns for the manufacturing sector within the automotive industry in 2024, according to the Allianz Risk Barometer. The report, based on insights from over 3,000 risk management professionals and business leaders, highlights the growing importance of addressing these risks to ensure business continuity and safeguard against potential disruptions.

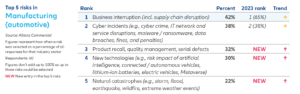

Despite a slight easing of post-pandemic supply chain disruption in 2023, Business interruption continues to hold its position as the number one threat for automotive manufacturing, with 42 percent of respondents expressing concern. Cyber incidents and natural catastrophes are the top two causes of business interruption feared most by companies, followed by fire and machinery/equipment breakdown or failure.

These results underscore the interconnectedness and volatility of the global business environment, as well as the reliance on supply chains for critical products or services. Consequently, improving business continuity management, identifying supply chain bottlenecks, and developing alternative suppliers remain key risk management priorities for companies in 2024.

The COVID-19 pandemic and its subsequent disruption to supply chains have served as a wake-up call for companies. Compared to pre-pandemic times, businesses are now better prepared for business interruption or supply chain events. According to the Allianz Risk Barometer, the most common actions taken to de-risk supply chains include developing alternative suppliers (60 percent of responses), improving business continuity management (42 percent), and identifying and remediating supply chain bottlenecks (37 percent).

According to the Allianz Trade’s Automotive sector risk report, the automotive market is expected to normalize this year as demand loses momentum following a strong rebound in 2023. The growth of new auto registrations is expected to slow down to +1.9%. New auto registrations saw a significant recovery in 2023 as Covid-induced supply-chain disruptions eased, and pent-up demand released. Additionally, resilient economic growth and strong, albeit slowing, growth in EVs fuelled car sales – total global auto registrations increased by +11.3 percent to nearly 88mn, though is still below pre-pandemic levels.

For the second consecutive year, Cyber incidents rank as the second most important risk in automotive manufacturing, with 38 percent of respondents expressing concern. The recent surge in ransomware attacks saw insurance claims activity increase by over 50 percent compared to 2022. Hackers are increasingly targeting IT and physical supply chains, launching mass cyber-attacks, and finding new ways to extort money from businesses. As a result, early detection and response capabilities and tools are becoming increasingly crucial. Investment in detection backed by artificial intelligence is expected to enhance incident identification. Without effective early detection tools, companies may experience longer unplanned downtime, increased costs, and a greater impact on customers, revenue, and reputation.

“Cyber criminals are exploring ways to use new technologies such as generative artificial intelligence (AI) to automate and accelerate attacks, creating more effective malware and phishing. The growing number of incidents caused by poor cyber security, in mobile devices in particular, a shortage of millions of cyber security professionals, and the threat facing smaller companies because of their reliance on IT outsourcing are also expected to drive cyber activity in 2024, “explains Santho Mohapeloa, Cyber Insurance Expert, Allianz Commercial.

Product recall, quality management, and serial defects emerge as a new risk at #3 with 32% of respondents identifying it as a concern. The automotive sector bears the brunt of product recall losses, accounting for over 70% of the value of all losses. The increasing complexity of supply chains and stricter regulations contribute to the rising impact of product recalls on companies’ financials and reputations. With recalls affecting a higher number of units, driven by factors such as faster speed-to-market and outsourcing of research and development, the automotive sector remains a frequent driver of claims.

As the automotive manufacturing sector faces these risks head-on, companies must prioritize risk management strategies and enhance their resilience. By proactively addressing Business interruption, Cyber incidents, and Product recall risks, companies can safeguard their operations, reputation, and bottom line.

Allianz Risk Barometer

The Allianz Risk Barometer is an annual business risk ranking compiled by Allianz Group’s corporate insurer Allianz Commercial, together with other Allianz entities. It incorporates the views of 3,069 risk management experts in 92 countries and territories including CEOs, risk managers, brokers and insurance experts and is being published for the 13th time.